China’s Export Controls on Critical Minerals – Gallium, Germanium and Graphite

- 23 de May de 2024

- Posted by: ap.jailsonpereira@gmail.com

- Categories: Business plans, News

On August 1, 2023, China began restricting exports of gallium and germanium, followed more recently, on December 1, with new export controls on high-grade graphite. China has justified these measures on the grounds of national security; however, gallium and germanium have broad applications in a range of industries, including electronics and fiber optics, while graphite anodes are an essential component of the lithium-ion batteries used in electric vehicles.1

The U.S. Department of Energy categorizes each of these materials as a critical material, highlighting their strategic importance to economic, energy independence and/or national security.2 While the initial market reaction to the restrictions on gallium and germanium was moot, China’s action on graphite poses a significant risk to the stability of electric vehicle supply chains and highlights the fragility of dependence on critical materials from China.3 This article explores developments surrounding the announcement of restrictions, as well as the role of gallium, germanium and graphite in U.S. supply chains, and potential implications of China’s export restrictions.

The Export Control Policy

Chinese export controls on gallium and germanium are already in play, and the controls on certain graphite products, specifically high-purity synthetic graphite and natural flake graphite, were slated to take effect on December 1. Products falling under the new controls cannot be exported from China unless approval is obtained through China’s Ministry of Commerce. The Ministry has the authority to issue export licenses to applicants for the materials in question. In practice this will place China’s supply of designated gallium, germanium and graphite products designated for export to other countries firmly under the control of the Chinese government while also allowing for flexibility on how tightly such exports are controlled.4

These recent restrictions are broadly seen as a response to prior actions that have impacted semiconductor exports to China from the United States, Japan and the European Union: the new graphite restrictions came just days after the U.S. Department of Commerce released a package of rules designed to update the export controls on advanced computing semiconductors, semiconductor manufacturing equipment and supercomputing items to countries of concern, including China.5 The recently imposed and announced critical mineral export controls will enable China to control export destinations and end-use applications while also fostering a domestic supply chain in the related mid- and downstream sectors for gallium, germanium and graphite products. Although China has a significant trade surplus in upstream raw materials, the country has a substantial deficit in downstream products, including power electronics and sensors, for example.

Supply Chain Landscape

Markets for Gallium, Germanium and Graphite

- Gallium & Germanium: Gallium and germanium are primarily used for end-to-end error control in a range of technology applications and industries, including telecommunications, that are large consumers of these materials. Gallium and germanium are critical materials, given their importance as industrial inputs and their lack of direct substitutes. Alternatives for germanium exist but result in significant performance losses; there is no practical substitute for gallium’s various technology applications. China is the primary producer and exporter of gallium and germanium; the United States has become a major consumer and importer, and demand is expected to continue to grow.

- Graphite: As noted, graphite is essential for the electric vehicle (EV) supply chain. While a multitude of materials, including critical minerals, are employed in the production of EV batteries, graphite is commonly used for the anode and is the largest component by weight, regardless of the cathode chemistry.6 Surging demand for graphite from the EV sector has triggered apprehension that there could be shortages of the material over the near term.7 Given this context, China’s recent actions have caused more uncertainty for global EV supply chains. Graphite consumption in the United States tops that of gallium and germanium combined. In 2022, the U.S. consumed 72,000 tons of graphite – all of which was imported and a third of which came from China.8 These volumes are only expected to grow, given the surging demand for EVs and associated components.

Upstream Supply Landscape

As of 2022, China was responsible for 98% of primary low-purity global gallium production, 60% of global germanium production and a majority of the world’s graphite production.9 China’s market share may diminish as a result of its recent actions.

- Gallium & Germanium: Despite having a low share of natural deposits globally, China has a firm grip on the gallium market. Natural deposits of the metal are spread across the globe, but the substantial investment in refinement required for production of gallium pose significant constraints; only a handful of companies around the world have the capacity to produce the high-purity quality needed.10 As gallium is essential in the realm of military technology, China’s trading partners will need to diversify their sources of supply through direct mining, direct manufacture, direct refining or production, or via equipment recycling.

The germanium market is more competitive globally, and several countries could seek to increase market share as a result of China’s actions. Outside of China, major players include Canada, Finland, Russia and the United States, which account for the remaining ~40% of total germanium production.11 Since there are abundant natural deposits of germanium in Canada and the United States, these two countries are well positioned to step into potential gaps in supply. Producers outside of China will most likely not need to explore the primary production of germanium, given that the mineral can be produced as a byproduct of readily abundant and easy-to-process zinc. - Graphite: China is the dominant supplier of natural and synthetic graphite globally. Natural graphite is mined and processed through ore deposits that are broadly dispersed across the globe. Despite only accounting for ~16% of the world’s known reserves, China accounted for 65% of production in 2022.12 Ukraine (27%) and Canada (22%) boast larger reserves than China but account for less than 2% of global production combined. China controls the synthetic graphite market, comprising as much as 98% of the world’s supply.13 The United States, despite its ambitious EV manufacturing aspirations, has a diminutive amount of the world’s known reserves of natural graphite and is not a meaningful producer of synthetic graphite. It is unclear how tightly graphite exports will be limited or how excess demand will be met; however, China’s recent restrictive measures will add impetus to and accelerate the build-out of graphite mining and broader supply chains outside of China that are already underway.

Market Implications

Impact on Industry

- Gallium & Germanium: The immediate reaction to China’s decision to restrict the export of gallium and germanium was somewhat moot, as demonstrated by the marginal increases in associated commodity prices since the announcement in July.14 Initially, exports of gallium and germanium products from China ground to a halt, with customs data showing zero export clearance of covered products in August.15 It has been reported, however, that exports resumed in September as major producers in China were granted the necessary export licenses.16 As seen with other commodities in the past, such measures tend to result in discrepancy between prices in China and other markets.

In the short-term, it appears that the Chinese government will continue to restrict the flow of gallium and germanium. It is not clear how many exemption licenses have been provided and at what volumes, but there has been a clear reduction in exports over earlier levels. This will likely result in the lowering of the global supply of these critical minerals and thereby lead to increases in pricing. Producers in China that benefit from export exemptions, as well as producers in other markets and recycling operations with high germanium and gallium content, will be best positioned to take advantage of these market and pricing dynamics. Over the medium term, the export controls on gallium and germanium could affect a number of sectors including telecommunications and power electronics, given the importance of these materials for a broad array of microchips and devices integral to 4G, 5G and other wireless networks, as well as for inverters, converters and other power regulators and control equipment for renewable energy and energy storage systems. - Graphite: The impact of the export controls on graphite could be much greater, depending in large part on the actual degree of restrictions applied by China. If an aggressive approach is taken and restrictions are heavily applied, we would expect the measures to depress prices for graphite and battery anode material in China and inflate delivered prices for importers in the United States, Europe and elsewhere. Over the medium term, restrictions could severely reduce available graphite supply for EV battery manufacturers in the United States, Europe, South Korea and Japan. This in turn would keep upward pressure on the price of synthetic and natural graphite exports, while domestic Chinese prices for graphite flake could decline as a result of oversupply.

From an industry perspective, EV market participants outside China could be affected severely, given that graphite is the key input for EV battery anodes. Overall, the recently announced restrictions could hamper the EV sector and lead to supply shortages and bottlenecks as well as substantial cost increases. The move highlights the significant leverage China has with regard to critical materials, as well as the potential ramifications of escalating trade tensions. Not only could material restrictions on graphite exports disrupt the rapid deployment of electric vehicles and thereby undermine decarbonization efforts, the impact could be felt more broadly, given the use of graphite in a range of applications, including advanced semiconductors. Ultimately China’s approach allows for a great deal of flexibility while maintaining an effective hold on high-grade graphite supply that can be tightened or loosened at will. - Implications: Longer-term, if there is no fundamental decoupling of the United States and China relations, supply and demand of gallium and germanium will likely adjust to the recently imposed export controls. Physical commodities tend to find a home as they flow through different markets, as observed with the bans on Russian oil and Australian coal. The recently announced export controls on high-purity graphite could be more problematic. Should China seek to aggressively restrict exports, it could result in near-term supply shortages and, over the longer run, more expensive graphite-based materials outside of China. The early stages of implementation will be key in determining how great an impact the controls are likely to have. However, given the nature of the policy, the threat to EV supply chains will remain in place, irrespective of how aggressively restrictions are implemented.

In light of the ongoing geopolitical and trade tensions, the United States is keen to prioritize alternative sources of supply for these critical minerals, including domestic production, as well as develop alternative materials to diversify supply away from China. Existing and aspiring producers in the United States can expect support from government funding administered through the Department of Defense’s Defense Production Act Investments Program and the Department of Energy’s Critical Minerals & Materials Program. Incentives such as the 48X manufacturing tax credit under the Inflation Reduction Act are also available for gallium, germanium and graphite producers and can be employed to offset intensive upfront capital expenditures. Because the United States is highly dependent on China for gallium, germanium and graphite, it will continue to prioritize diversification of supply of these and other critical materials in order to mitigate risk to supply chains.

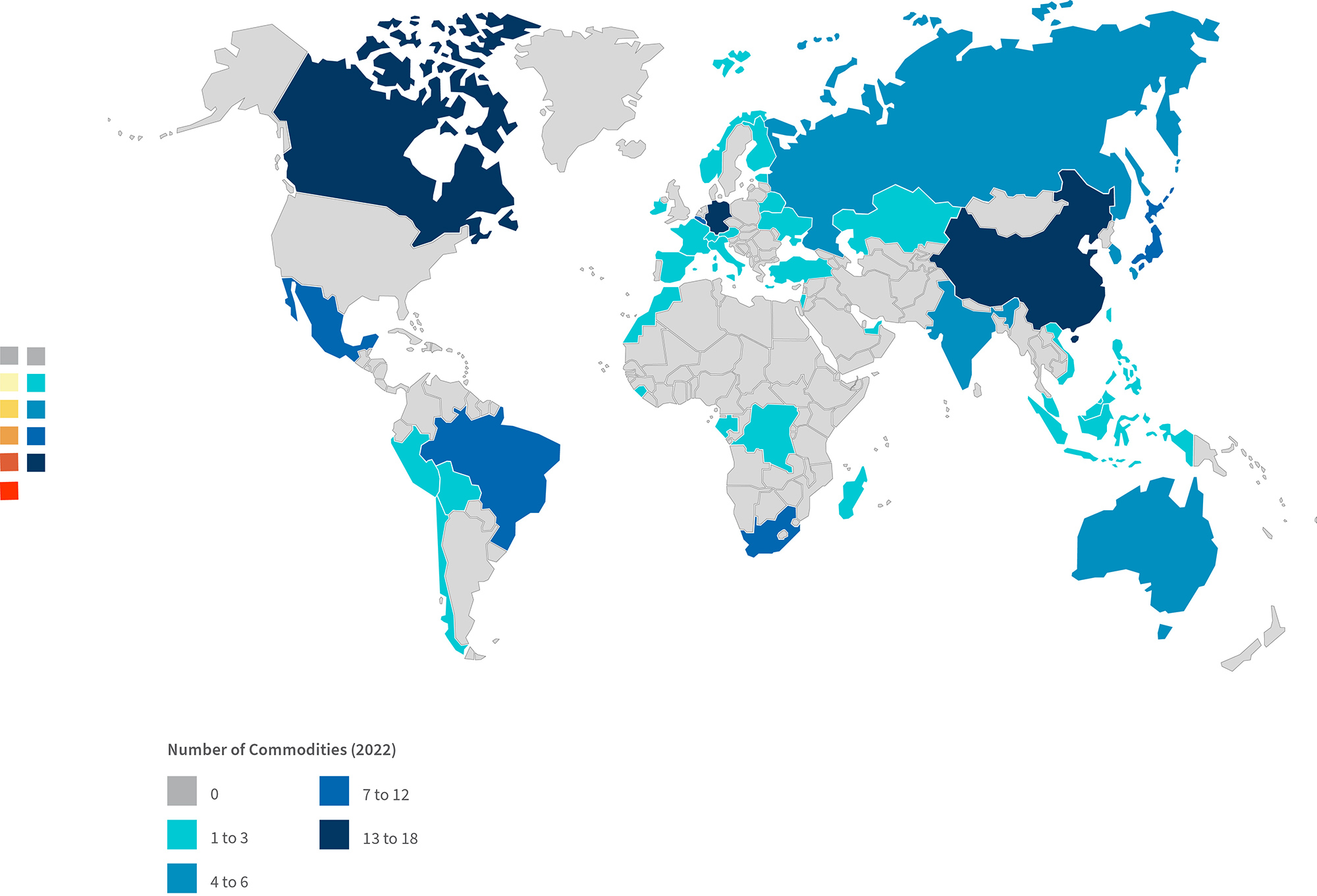

Figure 1 – Major Import Sources for Which the U.S. Was Greater Than 50% Net Import-Reliant in 202217

Source: USGS, Mineral Commodity Summaries, January 2023

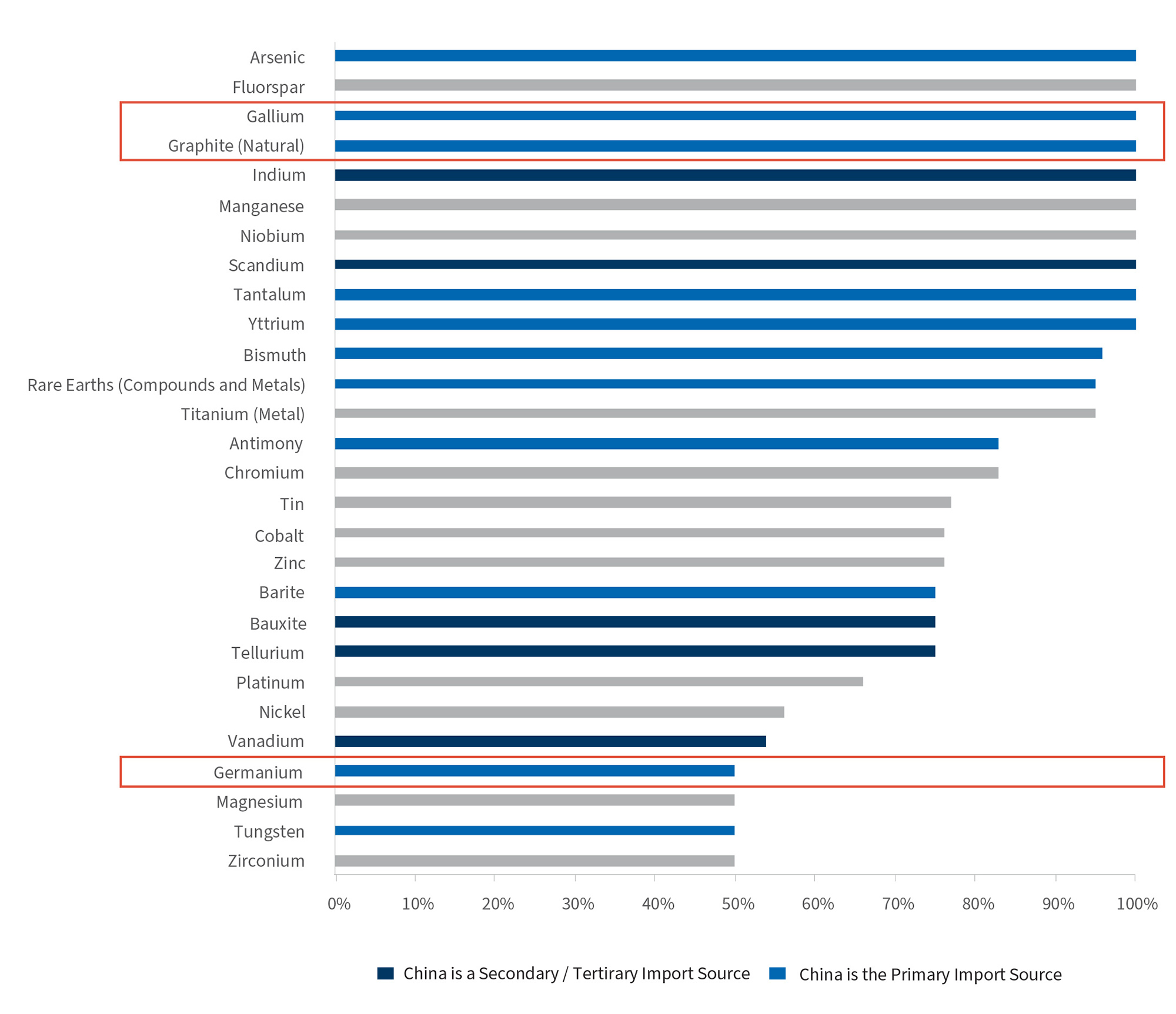

Figure 2 – Net Import Reliance (as % of Consumption)18

Source: USGS, Mineral Commodity Summaries, January 2023

Conclusion

China’s imposition of export controls on gallium and germanium was a shot across the bow that highlighted the fragility of international supply chains and their dependence on that country for the supply of many critical materials. China’s more recent move on graphite underscores the current trade dynamics and is all-the-more concerning. Depending on their implementation, these recent measures have the potential to disrupt global supply chains, hamstring critical industries, and encumber electrification and decarbonization efforts. Moreover, China has the ability to expand restrictions beyond those in place or announced currently, most notably in the domain of rare earth materials. While we believe this is unlikely, it nevertheless poses a major threat and the ramifications of such a development would be severe.

These recent developments raise the question as to whether the United States and other countries can become less dependent on critical mineral exports from China. U.S. domestic production of germanium, gallium and graphite is likely to increase over the medium to longer-term, given this is a policy priority and government incentives are in place to encourage growth; however, because of the amount of time and capital needed to bring new capacity online, a short-term supply deficit may emerge. The most likely outcome over the near term is a reconstructed supply chain that relies on friendly, stable trade partners outside of China that have ample critical mineral supply, such as Canada and Australia — suggesting that China could be at least partially displaced and end up being adversely affected by its own export controls. As we have seen with China’s recently lifted ban on Australian coal imports, trade restrictions can have unintended consequences. With its recent actions, China has demonstrated its importance in the realm of critical and rare earth materials and underlined the need for countries and corporations alike to shore up and diversify their supply chains, to the extent possible, to mitigate this inherent threat. The next months will reveal the extent of China’s implementation of the restrictions as well as the countries and entities being targeted; however, while a light-handed approach is possible, the warning shot has been fired and the need for more stable, localized supply chains will be all the more important going forward.

How We Can Help

Trastamaris’s Power, Renewables & Energy Transition (PRET) practice helps clients across the value chain navigate the energy transition by providing a wide array of advisory services addressing the strategic, financial, operational, reputational, regulatory and capital needs of our clients. We supply tailored services for leading market participants, assisting across all stages of an engagement. We offer deep experience advising across the supply and value chains in the energy transition sector, including performing commercial, financial, operational and regulatory due diligence as well as advising on supply chain strategy.

We take a holistic and integrated approach to identifying and managing sourcing risks and supply markets and by identifying cost take-out opportunities that can help capture savings to offset potential price increases caused by market conditions. We also support companies and stakeholders in communicating these risk management strategies and addressing concerns with investors, customers and policymakers.

Footnotes:

1: Emily Benson, Thibault Demaniel, “China’s New Graphite Restrictions,” Center for Strategic & International Studies (October 2023).

2: Diana J. Bauer, Ruby T. Ngyuen, Braeton J. Smith, “Critical Materials Assessment,” U.S. Department of Energy (July 2023).

3: Jason Rogers, Ailing Tan, Winnie Zhu, Sybilla Gross, “China Allows a Trickle of Critical Minerals Exports Ahead of Graphite Curbs”, Bloomberg (November 21, 2023).

4: Jason Rogers, Ailing Tan, Winnie Zhu, Sybilla Gross, “China Allows a Trickle of Critical Minerals Exports Ahead of Graphite Curbs”, Bloomberg (November 21, 2023).

5: “Commerce Strengthens Restrictions on Advanced Computing Semiconductors, Semiconductor Manufacturing Equipment, and Supercomputing Items to Countries of Concern,” Bureau of Industry and Security (October 17, 2023).

6: Govind Bhutada, “The Key Minerals in an EV Battery,” Visual Capitalist (May 2022).

7: “Global graphite investment horizon outlook – Q3 2023,” Wood Mackenzie (September 29, 2023).

8: “Mineral Commodity Summaries – Graphite,” USGS (January 2023).

9: “Mineral Commodity Summaries – Gallium,” USGS (January 2023); “Germanium,” Critical Raw Materials Alliance (December 2023).

10: “Gallium,” Critical Raw Materials Alliance (December 2023).

11: “Germanium,” Critical Raw Materials Alliance (December 2023).

12: “Mineral Commodity Summaries – Graphite,” USGS (January 2023).

13: “Mineral Commodity Summaries – Graphite,” USGS (January 2023).

14: “Germanium Ingot Price and Gallium Price,” Shanghai Metals Market (September 2023).

15: Challey, “China’s gallium and germanium exports were zero in August,” EE Times China (September 26, 2023).

16: Sun Le, “AXT’s Chinese Subsidiary has Obtained a Preliminary Export License for Gallium Arsendinde/Germanium Substrates”, IJiWei (September 2023).

17: “Mineral Commodity Summaries,” USGS (January 2023).

18: “Mineral Commodity Summaries,” USGS (January 2023).

Leave a Reply

Contact us at the Trastamaris office nearest to you or submit a business inquiry online.